Filing your first tax return is a major financial milestone, but it often comes with more questions than answers. Between understanding your filing status and tracking down various 1099 forms, the process can feel overwhelming.

Proper preparation is the difference between leaving money on the table and maximizing your refund. In this guide, our experts break down the essential steps for first-time filers to stay compliant and keep more of what they earn.

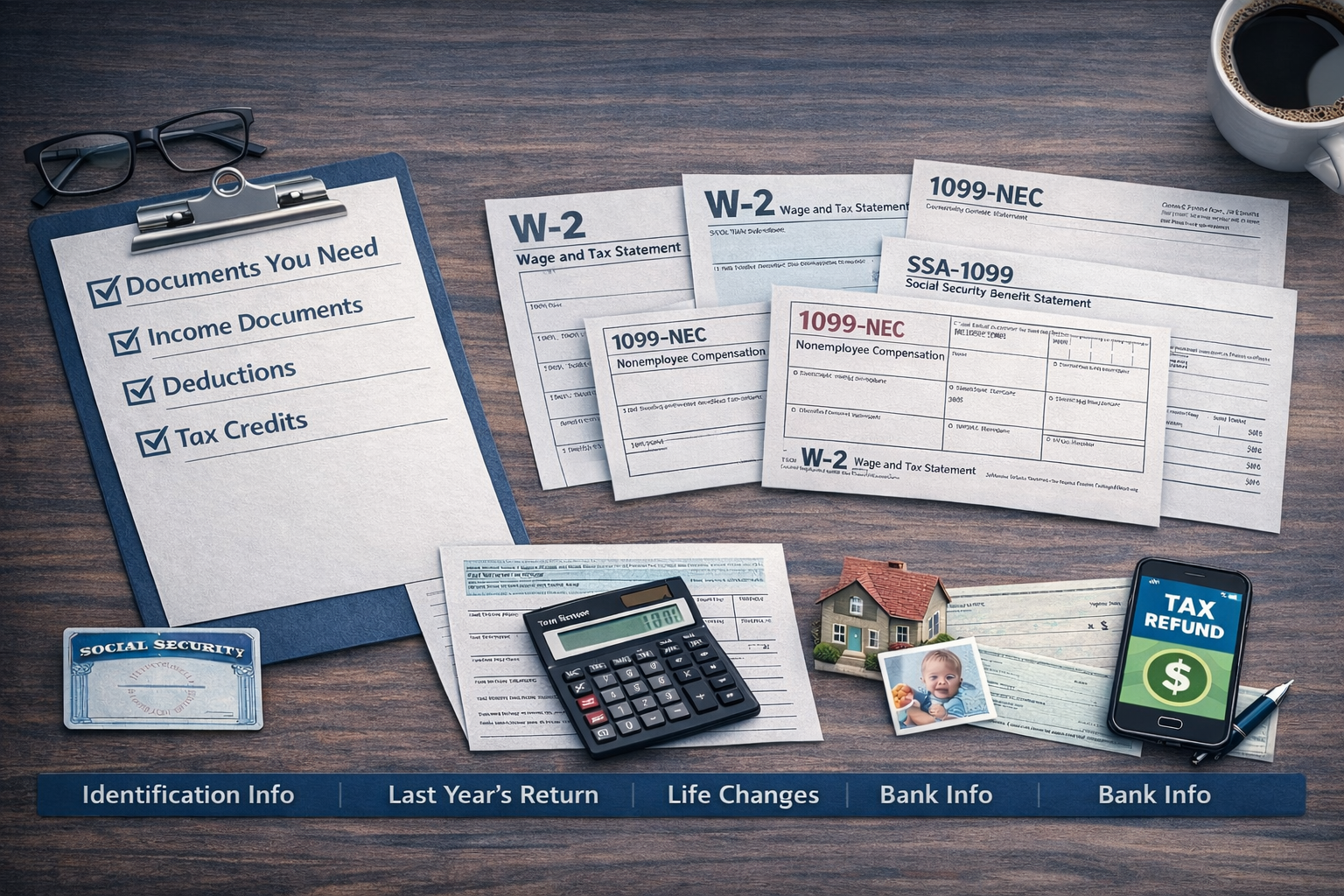

1. Gather Your Essential Tax Documents

Before you start your return, you need to collect proof of income and expenses. The IRS receives copies of most of these forms, so accuracy is non-negotiable to avoid “red flags.”

Common Income Forms:

- Form W-2: If you are a traditional employee, this shows your total earnings and the taxes already withheld.

- Form 1099-NEC: For those who did freelance, gig, or contract work.

- Form 1099-INT/DIV: To report interest from savings accounts or dividends from investments.

- Form 1099-G: For government payments, such as unemployment compensation.

Expense Records:

If you plan to itemize deductions or are self-employed, you will also need:

- Bank and credit card statements.

- Receipts for charitable donations or medical expenses.

- Records of business-related expenses (mileage, equipment, home office).

2. Determine Your Filing Status

Your filing status is the “anchor” of your tax return. It dictates your tax bracket, your tax rate, and the Standard Deduction you are eligible for.

The five filing statuses are:

- Single

- Head of Household (Generally for unmarried individuals with dependents).

- Married Filing Jointly

- Married Filing Separately

- Qualifying Surviving Spouse

Pro Tip: Before filing, ensure your parents or guardians aren’t claiming you as a Dependent. If they claim you, it changes how you must file your own return.

3. Special Rules for Freelancers & Side-Hustlers

The “Gig Economy” has changed how young people work. If you repair computers, babysit, or drive for a ride-share service, the IRS views you as an Independent Contractor (Sole Proprietor).

- The $400 Threshold: You must file a return if your net earnings from self-employment were $400 or more.

- Self-Employment Tax: Unlike traditional employees, you are responsible for the full 15.3% for Social Security and Medicare.

- Estimated Payments: If you expect to owe more than $1,000 in taxes, you may need to make quarterly estimated payments via Form 1040-ES.

4. Maximize Your Deductions and Credits

Don’t miss out on “tax breaks” that can significantly reduce your bill or increase your refund.

Tax Deductions (Reduce your taxable income):

- Student Loan Interest: You can often deduct interest paid on qualified student loans.

- Home Office: Available only for independent contractors using a dedicated space for work.

- Charitable Gifts: Even small donations to 501(c)(3) organizations count.

Tax Credits (Dollar-for-dollar reduction of tax owed):

- American Opportunity Tax Credit (AOTC): For the first four years of post-secondary education.

- Lifetime Learning Credit (LLC): For professional degree courses or job-skill improvement.

- Earned Income Tax Credit (EITC): A refundable credit for low-to-moderate-income working individuals.

5. Avoid Costly Penalties

The IRS is strict regarding deadlines. For the 2025 tax year, the filing deadline is April 15, 2026.

- Failure-to-File: This penalty is 5% of the unpaid taxes for each month the return is late.

- Failure-to-Pay: This is 0.5% of the unpaid taxes for each month the tax remains unpaid.

Should You Hire a CPA for Your First Return?

While free software exists, it often misses the nuances of complex situations like crypto trading, multi-state income, or side-hustle deductions. A CPA doesn’t just “file papers”—we provide a strategic roadmap to ensure you are paying the legal minimum and avoiding audits.

Ready to file with confidence? Contact our team today to schedule a consultation and ensure your first tax season is a success.